How a Credit Dispute Can Hurt Your Mortgage Application

There is a recent change in mortgage underwriting that is killing some mortgage applications dead in their tracks or at least delaying the process by a few more weeks. If you have ever filed a Consumer Statement with a credit bureau to dispute an account’s status, then that Consumer Statement may very well cause your mortgage application to be turned down by the Automated Underwriting Systems (AUS) that all mortgage lenders now use.

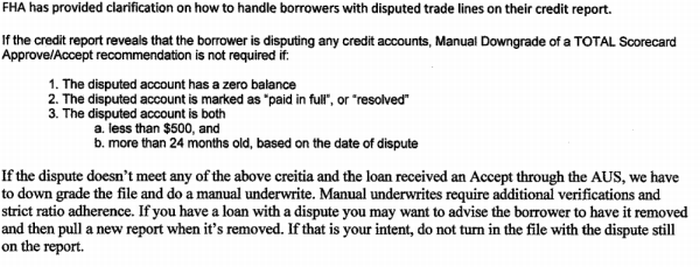

At my company, we have seen several recent examples of loans that should have received an “Accept” rating from the AUS, only to receive a “Refer” rating instead. (In a practical sense, a “Refer” rating is the same thing as a “decline”.) Eventually, when the Consumer Statement was removed from the credit report, most of those files received the “Accept” rating. What follows below is the guidance that our Underwriting Dept. recently gave us about this matter as it pertains to FHA loans in particular…

Translation: If you file a Consumer Statement with the credit bureaus to dispute an item, get this item resolved and/or cleared up before you apply for a mortgage!

To clarify, though, this guidance specifically deals with items that you add a Consumer Statement to. The normal process to dispute items on your credit report is not a problem and it is not affected by this current underwriting guidance.

Need more credit tips? Get your free copy of “101 Fast Fixes to Boosting Your Credit Score” here.